What Challenges Does Covid-19 Continue to Bring?

A Backdrop of Considerable Uncertainty

What challenges does COVID-19 continue cue to bring?

Why is the Industrial & Logistics sector continuing to grow?

Find out how five sectors of the property market have performed in Q3

It would have been nice if, unlike the last two market updates, the focus was on something other than the Covid-19 pandemic. However, just when things started to look more positive the dreaded second wave has become a reality and new restrictions introduced across the UK, are likely to further damage the economy.

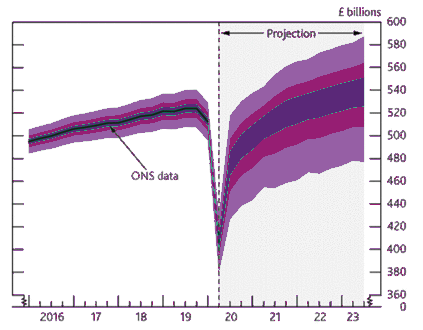

The Bank of England is now predicting that GDP will return to pre-crisis levels towards the end of next year (see below) but the next 12 months will depend on the evolution of the pandemic, further measures taken to protect public health and how governments, households and businesses respond to all these factors, not to mention Brexit and the result of the US election.

Bank of England UK GDP Projection

Source: The Bank of England

The UK property Market

General

Unsurprisingly the lockdown drove investment volumes down to a record low in Q2 with total UK investment volumes reducing to £3.6bn which is around 75% below the five-year quarterly average (according to LSH). What is more positive is that investment volumes did increase throughout the quarter with volumes in June reaching £1.6bn, almost twice the level seen in May.

There are huge sector variances however, industrial remaining the sector of choice with yields moving in by 25bps, but a continued upward trend on yields (i.e. a reduction in value) in the retail sector which is still being hit hard by a decrease in footfall, particularly in shopping centres and high street retail.

.jpg)

Industrial

The industrial and logistics sector has emerged as a clear winner from the Covid-19 pandemic and with this has come a significant increase in both institutional appetite and occupational demand, particularly for logistics.

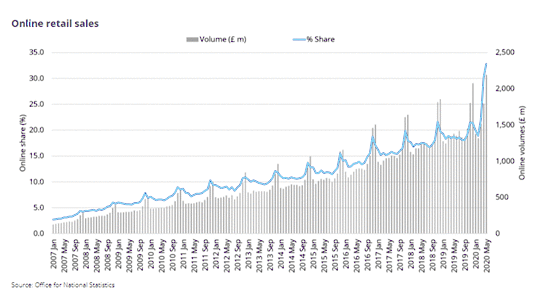

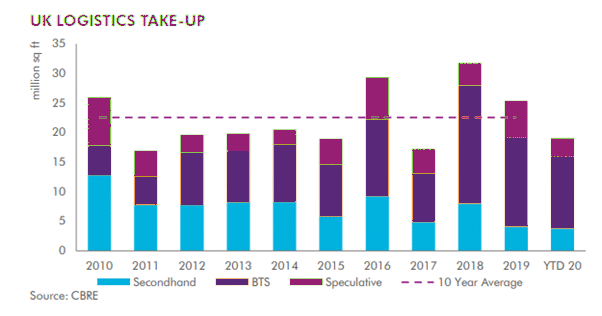

Behavioural changes due to lockdown have resulted in a significant shift in online sales which have risen to 33% of total retail sales and are unlikely to ever go back to pre-pandemic levels. This has led to a surge in demand for well-located distribution warehouses, which Barwood Capital Funds are well placed to benefit from, with record take up in H1 2020 of 19.1m sq ft (see bar chart below which shows only first six months for 2020).

With the changing fortunes of retail and logistics, opportunities are already starting to emerge including the repurposing of retail warehousing to urban logistics and multi let estates. With land prices for logistics property reaching record levels, it is likely that savvy investors will look to opportunities like these, to find value in the sector. This is an area of the market that Barwood Capital is currently tracking closely and with our strong regional network, we are very well placed to take advantage of any opportunities. A good example of this is the ex B&Q warehouse we have recently acquired on behalf of Growth Fund IV. https://barwoodcapital.co.uk/news/we-b-qed-it-in-sheffield

Industrial and logistics remains the favoured sector from a fund performance perspective and this is unlikely to change in the short to medium term. Rental growth in the sector is still forecast to be strong over the coming years and Colliers estimate that total returns will grow to 6% in 2021 and average 5.6% over the five-year forecast.

The multi let industrial sector has continued to prove itself to be resilient to market fluctuations with rent collections remaining healthy and some areas are experiencing continued rental growth. Barwood Capital’s multi let industrial portfolio has had rent collections of over 90% for Q2 and Q3, with few tenant failures. While the second wave and the end of furlough is undoubtedly a risk, so far, the sector has performed well, and rental and capital growth is predicted to return in 2021.

Source : LSH

Vacancy rates in the multi let sector have seen a steady decline since 2011 driven by increasing occupier demand and high retention rates from a diversified occupier base. Due to a higher cost of build of small units, the multi-let sector has also seen a reduction in supply and a severe lack of new stock. The disjointed supply and demand dynamics in this sector are creating upward pressure on rents and increased investor demand, which our multi let portfolio is well placed to take advantage of.

The Office Sector

There are likely to be structural changes to the office sector going forward with lockdown accelerating the already emerging trend of flexible working and hot desking. This could be to the benefit of regional offices as companies look to move out of London and to areas less reliant on public transport.

Pre-pandemic, there was a shortage of grade A space in the regions with analysis from Savills showing that rents haven’t fallen across the ‘big six’ markets since 2007 and the current vacancy rate is only 7.5%, the lowest on record. The graph below demonstrates vacancy across the whole of the regional market is also at an historic low of below 10%.

.jpg)

While there is a total available office supply of 11.3m sq ft in the UK regional office markets, this is a 17% decrease since the end of 2019 and of that only 3m sq ft is grade A which only reflects 11 months of take up. This indicates a major under supply of grade A office space outside London, so despite the structural change in the market this could be a sector to watch, particularly in the regions.

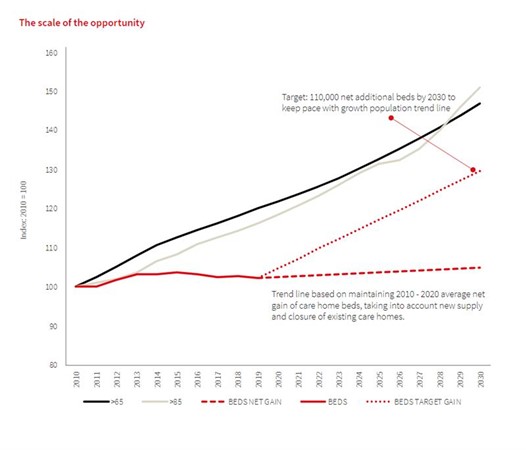

Alternatives – The Care Sector

The Covid-19 pandemic has highlighted the need for investment and innovation in the UK healthcare property sector, particularly considering such a high proportion of UK care homes facilities’ (over 70%) are over 20 years old. This is leading to many operators upgrading their existing portfolio and fuelling a long-term upward trend in demand for new, purpose-built care homes. The graph below, produced by JLL, demonstrates the number of new beds needed to keep pace with the growing UK population.

Source: JLL

The annual UK Healthcare Development Opportunities 2020 research carried out by Knight Frank reports that while the number of care home beds increased by 2,500 in the last financial year, the number of homes fell overall as smaller and outdated care homes closed while larger, purpose-built care homes or existing homes added new beds to create more efficient and viable schemes. Our care home partner, Perseus Land and Developments, has so far secured seven schemes on behalf of Barwood Capital Funds and has already achieved planning consent for purpose-built care homes on three of these. Through the extensive knowledge and experience at Perseus, the team are able to pinpoint the regional areas with the greatest undersupply and bring land through the complex planning system, unlocking significant value by creating consented sites.

Retail

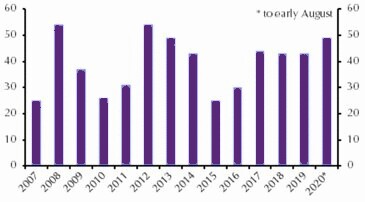

The retail sector continues to be a victim of a huge drop in consumer demand for physical retail with the shift to online being hugely inflated by Covid-19. This has led to an increase of CVA’s and store closures particularly on the high street and in shopping centres. Figures in the graph below demonstrate the number of administrations for only the first seven months of the year. They were already higher than those for full previous years.

Retail Administrations

Source : Capital Economics

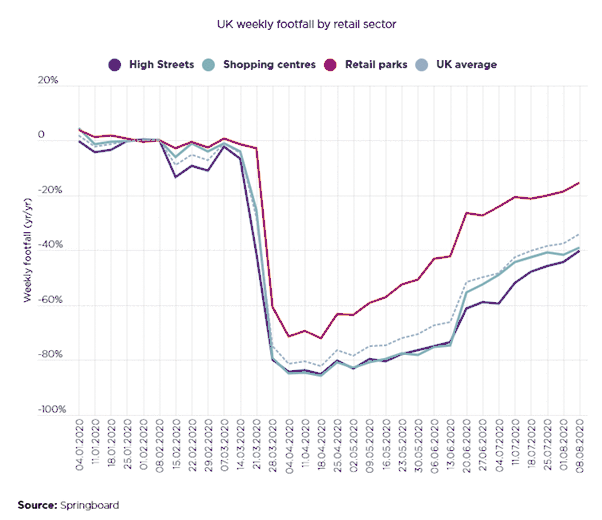

High streets and shopping centres have though experienced a marked improvement to weekly footfall flowing from the reopening of hospitality from 4th July. However, according to data produced by Springboard, despite this considerable weekly growth in footfall, high street destinations remain 40% below 2019 levels and shopping centres 39% below. Retail parks are doing slightly better, although still around 15.5% down.

With the ever-growing trend for more online shopping there is little good news in the sector and businesses without a strong online presence are likely to continue to face big difficulties.

Residential

The residential market has fared well in recent months with Halifax reporting that prices had bounced back to their highest ever level thanks to a mini-boom since lockdown, which saw annual price growth up 3.8% in July compared with the same month in 2019.

RICS UK residential market survey

The RICS UK residential market survey also reported that house prices were in positive territory for the first time since lockdown in March with a net balance of 12% of survey respondents reporting an increase in house prices (compared to -13% in June). Nationally, for properties listed at below £500K, 78% of respondents now report that sales prices are coming in at least level with the asking price.

According to Rightmove, the areas that have seen the biggest increase in demand are coastal and rural with more people moving out of urban areas. Optimum commute times are reported to have increased from 60 to 90 minutes as the number of days in the office reduces. The volume of property sales was still down in June (36% lower than the same period in 2019), but close to a third up on the month before. Mortgage approvals however more than quadrupled in June, reaching 40,010. The Barwood Residential Investment Platform (‘BRIP’) continues to see a significant interest in viewings and multiple reservations at asking prices over the last quarter which is perhaps unsurprising as its strategy of developing well located regional, family homes is exactly what is most in demand.

Conclusion

With a backdrop of considerable uncertainty, sector selection has never been more important. Barwood Capital’s investment strategy is focused on the industrial, retirement living and residential sectors and within these a focus on sites or assets where we can innovate, unlock and add real value, through planning, development, refurbishment and pro-active asset management.

Another key theme that is having an increasing impact on the market is sustainability. Next quarter we will explain our approach to responsible property investment and how we are ensuring that we are delivering strong and sustainable growth.